15 / 40

15 / 40

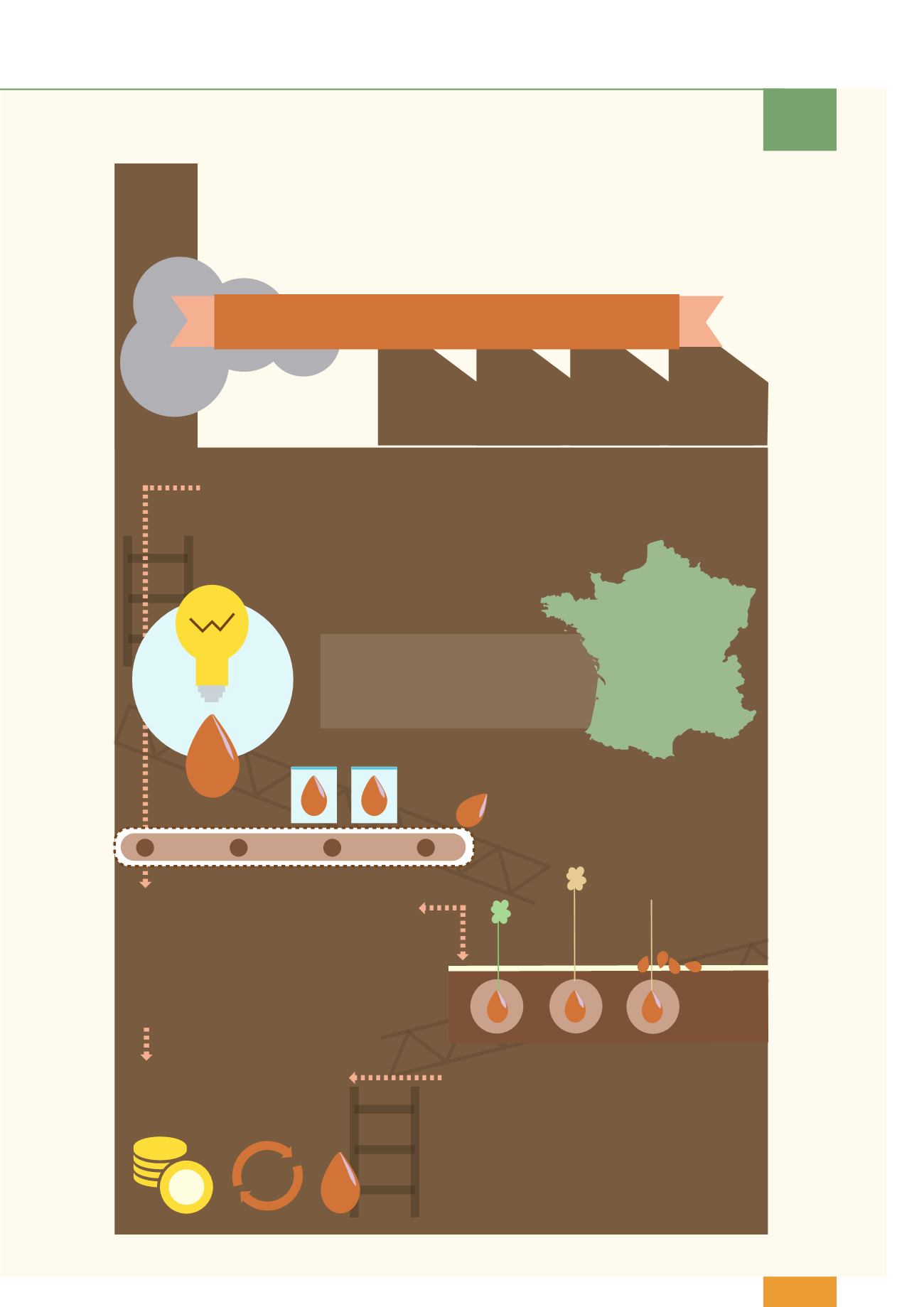

Concentration of market power

in the EU seed market

Seed growers /

Multipliers

Seed traders /

retailers

Production/treating

companies

At the beginning of the seed chain,they create new varieties

and produce seeds.

Breeders create the added value in the seed sector. Breeding companies own the

intellectual property rights on varieties, and bene t from the largest sales margins

on the products.

They produce seeds in their fields

from seed provided by production companies.

They sell seeds to farmers and other users.

They produce seeds most often under contracts

with seed growers.

They can also sort, process, package and market them. Many of the

enterprises involved are micro-enterprises located in Poland,

Hungary and Romania.

#2

#3

#4

only

72/565

of

seed enterprises

in France

(the world's leading

seed exporter and the EU’s

biggest seed market)

are actually

breeders

The number of seed breeders

is very small.

It is not possible to find out which of these

enterprises are independent

.

Among the 72 enterprises, Clause, Eurodur, Limagrain Europe

and Vilmorin SA belong to the same group. Some of the

enterprises are public bodies, such as INRA and CIRAD

.

€

Breeding companies

#1

THE STRUCTURE OF

THE SEED SECTOR

The seed sector is dominated by giant companies which over time have acquired smaller companies along the

seed supply chain, e.g. seed breeders, biotech research companies, etc. (vertical and horizontal integration).

They also very often establish alliances with other companies in the sector through outsourcing and partner-

ships. Additionally seed giants collaborate with each other in di erent ways (joint ventures, cross-licensing

agreements, etc.).

This means that large corporations operate throughout the whole seed chain.

15